Week of June 17, 2024 in Review

Both sales of existing homes and new construction were lower in May. Here are the highlights:

- Existing Home Sales Slower but Median Home Price at Record High

- Home Builder Sentiment Hammered Lower

- Housing Starts, Permits Lower Than Expected

- Flat Retail Sales Start of a Slowdown?

- Watching Trends in Jobless Claims

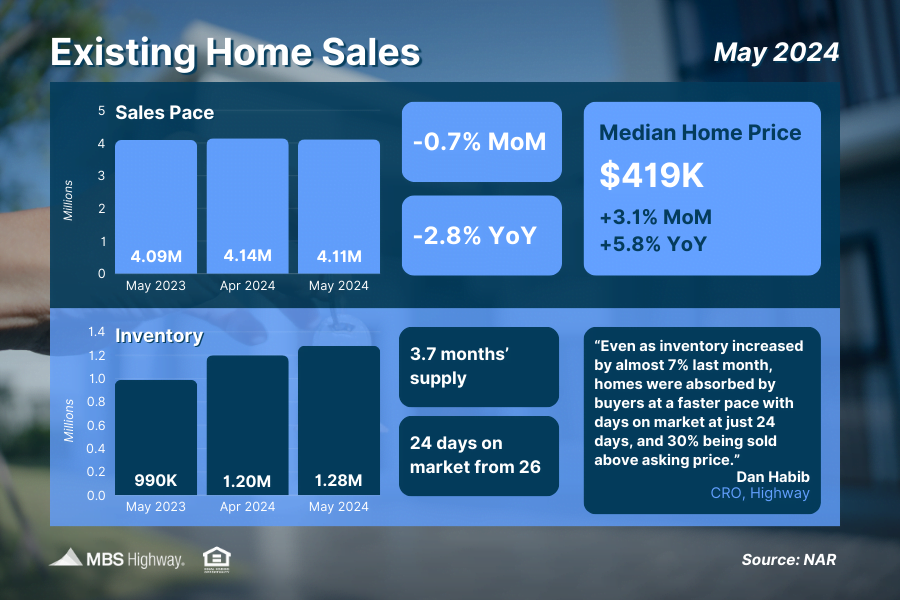

Existing Home Sales Slower but Median Home Price at Record High

Sales of existing homes fell 0.7% in May to a 4.1-million-unit annualized pace, per the National Association of REALTORS® (NAR), compared to the 1.4% decline the market was expecting. This report measures closings on existing homes in May and likely reflects people shopping for homes in March and April. The median home price reached a record high of $419,300, which was up 3% month-over-month and 5.8% year-over-year.

What’s the bottom line? While the pace of sales declined again in May, the speed at which homes sold continued to accelerate. Homes remained on the market for a shorter period in May, with the 24-day average down from 26 days in April. Plus, 30% of homes sold above list price, which rose from 27% in April. These factors both signal that demand and competition remain during this spring buying season, even in the face of elevated rates.

Inventory also saw a boost, as the 1.28 million homes available for sale at the end of May were up 6.7% from April and 18.5% from a year earlier. While this remains below healthy levels at just a 3.7 months’ supply at the current sales pace, rising inventory is certainly a step in the right direction to help improve ongoing supply constraints.

Home Builder Sentiment Hammered Lower

Confidence among home builders remains below the key breakeven threshold of 50, per the National Association of Home Builders (NAHB), as their Housing Market Index dropped 2 points to 43 in June. Any score over 50 on this index, which runs from 0 to 100, signals that more builders view conditions as good than poor.

Among the three index components, current and future sales expectations both entered contraction territory. The gauge judging buyer traffic also declined, remaining in contraction.

What’s the bottom line? NAHB’s Chair, Caril Harris, explained, “Persistently high mortgage rates are keeping many prospective buyers on the sidelines. Home builders are also dealing with higher rates for construction and development loans, chronic labor shortages and a dearth of buildable lots.”

Housing Starts, Permits Lower Than Expected

Housing Starts fell 5.5% from April to May, coming in well below what economists had forecasted. Starts for single-family homes, which make up the bulk of homebuilding and are the most crucial due to buyer demand, were also lower at a 5.2% decline. There was a similar trend in future construction, with Building Permits moving lower despite much needed supply.

What’s the bottom line? Softer than expected construction activity this spring could limit much needed supply down the road. This bodes well for appreciation and shows that opportunities remain to build wealth through homeownership.

Flat Retail Sales Start of a Slowdown?

There are signs that consumers are slowing their spending, as Retail Sales were only 0.1% higher from April to May. Sales in April were also revised downward from the originally reported flat reading to a 0.2% loss when compared to March.

What’s the bottom line? The pause in spending last month was a miss on estimates, as forecasters had predicted a 0.1% gain. The Fed will be closely watching future Retail Sales reports, as the strength of our economy will impact their monetary policy decisions this year.

Watching Trends in Jobless Claims

Initial Jobless Claims fell by 5,000 in the latest week as 238,000 people filed for unemployment benefits for the first time. Continuing Claims rose 15,000, with 1.83 million people still receiving benefits after filing their initial claim.

What’s the bottom line? While Initial Jobless Claims fell last week, they remain at elevated levels, with the latest reading the highest number of first-time filers in 10 months. Continuing Claims are also still trending near some of the hottest levels we’ve seen in recent years, suggesting that the pace of hiring has slowed. The Fed will be closely watching for any rising trends in unemployment claims as they weigh monetary policy and the timing for rate cuts, given their dual mandate and price stability and maximum employment.

Family Hack of the Week

June 26 is National Chocolate Pudding Day. This recipe courtesy of Taste of Home adds peanut butter for an extra special treat. Yields 8 servings.

In a heavy saucepan, combine 1 cup sugar, 1/2 cup baking cocoa, 1/4 cup cornstarch and 1/2 teaspoon salt. Gradually add 4 cups whole milk. Bring to a boil over medium heat; boil and stir for 2 minutes.

Remove from heat. Stir in 2 tablespoons butter, 2 tablespoons peanut butter and 2 teaspoons vanilla extract. Spoon into individual serving dishes and chill until serving. Garnish with whipped cream and chocolate shavings.

What to Look for This Week

More housing news is ahead, starting Tuesday with appreciation data for April from Case-Shiller and the Federal Housing Finance Agency. May’s New and Pending Home Sales follow on Wednesday and Thursday, respectively.

Also on Thursday, look for the final reading on first quarter GDP and the latest Jobless Claims. Friday brings a critical inflation update via the Fed’s favored measure, Personal Consumption Expenditures.

Technical Picture

Mortgage Bonds and the 10-year Treasury ended the week mostly unchanged as they have been the past week, and continue to trade sideways in wide ranges between support and resistance.

Mortgage-Backed Securities are between a tough overhead ceiling of resistance at 100.872 and a triple floor of support at the 100.427 Fibonacci level and 100 and 25-day Moving Averages.

The 10-year is also in a very wide range between support at 4.18% and overhead resistance at the 100 and 200-day Moving Averages.

We must remain on guard as MBS and Yields are susceptible to big price swings within these wide ranges. We will likely remain rangebound until some of the important economic data next week, highlighted by the Fed’s favorite measure of inflation, PCE (Personal Consumption Expenditures), which we think could come in lighter than estimates – More on that next week.